XH4D

Joby (NYSE:JOBY) is developing its own eVTOL (electric Vertical Takeoff and Landing) aircraft, which will be commercialized through both OEM sales and a UAM (Urban Air Mobility) service. The introduction of eVTOL aircraft is expected to drive enormous growth in the UAM market and Joby appears to be one of the leaders at this point in time. While this presents a large opportunity, there are also significant risks, both company specific (technology, regulatory) and market (demand, infrastructure).

Joby is probably the best opportunity in the space, but I tend to think that industry growth will end up falling well short of expectations. Despite this, the near-term path of the share price is likely to be dictated by financial conditions and Joby’s ability to smoothly progress through certifications and start up manufacturing operations.

Market

The UAM market is widely expected to rapidly expand in coming years, driven by growing traffic congestion problems and the advent of eVTOL aircraft, which offer advantages like lower emissions and less noise pollution.

Traffic congestion is a problem that is likely to get worse over time due to urbanization and the appeal of larger cities. Ridesharing and delivery are also contributing to increased traffic. As an example, traffic in LA has increased 80% since 1990. This situation is exacerbated by the fact that traffic in urban areas tends to be a radial flow convergence problem and that building new infrastructure in many countries has become extremely expensive.

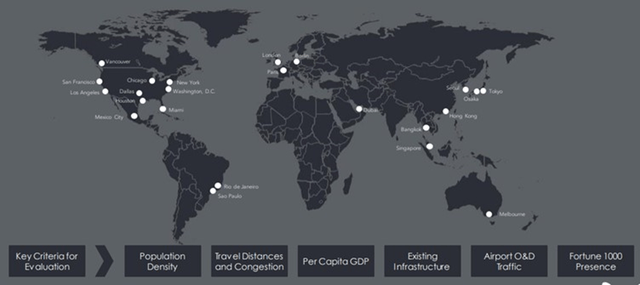

eVTOL aircraft can be up to 5x faster than driving in major metro areas, providing a major advantage over ground transportation in crowded cities. As a result, target markets will be densely populated urban areas that suffer from serious traffic congestion issues and have a relatively large population of high-income individuals or corporate travelers.

Figure 1: Joby Target Markets (source: Joby)

While this advantage has historically come at a large cost premium, eVTOL aircraft are expected to drive a significant reduction in costs. Blade has estimated a 14% reduction in costs for a typical flight, while Ark Invest has suggested that longer term prices could decline by more than 60%, although this is based on aggressive assumptions, particularly in relation to landing fees. Joby wants to offer flights at the same price as a ground-based taxi and estimates a $95 cost for a 25-mile trip compared to $393 for a twin-engine helicopter. Estimates on costs currently vary widely, in large part because eVTOL aircraft are still yet to be commercialized. In practice, costs will be highly dependent on landing fees, the manufacturing cost of aircraft, passenger load and aircraft utilization.

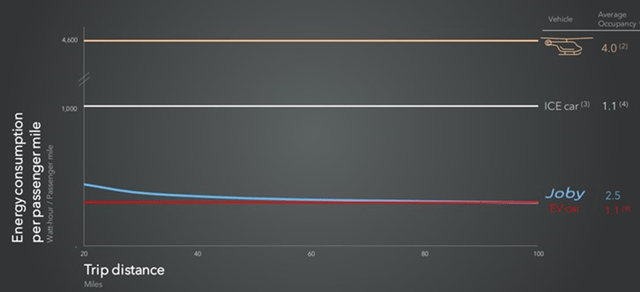

Figure 2: Joby Energy Consumption (source: Joby)

A reduction in costs is widely expected to help drive expansion of the market, although the actual impact of pricing may disappoint many. Route level price elasticity of demand for air travel has been estimated to be in the 1.2 to 1.5 range. In comparison, the price elasticity of demand for ride sharing is 1.35. Given the relatively high price point of UAM flights and the nascent state of the market, the price elasticity of demand is likely to be somewhat higher than these estimates.

More important is likely to be the fact that eVTOL aircraft produce less noise and emissions, potentially creating more acceptance in densely populated areas. Joby estimates that noise from its aircraft is 65 dBA when hovering at 100m, compared to approximately 93 dBA for a helicopter. This comes about because of the use of electric motors and because Joby uses a number of smaller rotors which have relatively low blade tip speeds.

Joby has suggested that its TAM in the US is around $500 billion and in excess of $1 trillion globally. In comparison, Blade (BLDE) has estimated roughly a $5-8 billion SAM for airport transportation across its initial target markets in the US. The bullish estimates for UAM will require widespread adoption and would likely cause pilot and infrastructure shortages.

Traffic congestion in the air will also likely become an issue at some point if the more bullish projections for the UAM market become a reality. This appears to be something that is largely overlooked at this point though. The busiest airport in the world handles roughly 100 million passengers annually and close to 1 million flights. To meet expectations, the busiest UAM markets would likely need to manage 1 to 2 orders of magnitude more flights.

Joby recently conducted an airspace simulation with NASA using real pilots and air traffic controller. The simulation focused on the Dallas-Fort Worth airspace and simulated scenarios with dozens of aircraft aloft simultaneously, along with existing airport traffic. Air traffic controllers were able to integrate up to 120 eVTOL operations per hour. While this level of traffic is broadly in line with Blade’s TAM estimates, it falls well short of more aggressive expectations. Beyond the necessary consideration for limits on traffic in the air, even a relatively modest increase in the number of flights will require new vertiports to be constructed in densely populated, high-wealth areas, which will likely be difficult to organize and extremely expensive.

Joby

Joby is a vertically integrated UAM company that wants to both sell aircraft and operate a UAM service. The company already has operational aircraft and is currently working its way through certification, with an eye on commercialization in the not-too-distant future.

Joby has designed an aircraft featuring:

- 150+ mile range

- 200 mph top speed

- 5 seats (1 pilot plus 4 passengers)

Of particular note for Joby is the high power to weight ratio of its motors and the fact that its aircraft do not need to utilize gearboxes to generate sufficient torque.

Joby has also designed and built its own charging system which actively cools the vehicle’s batteries, improving performance relative to off the shelf EV chargers. The right charging and thermal conditioning systems are critical to the success of UAM operations and for maximizing battery life.

Certification and Testing

Joby is pursuing a streamlined certification process with the FAA that will have global acceptability. The majority of the company’s components and tooling have been designed in-house though, which may create additional risk during the certification process. Joby has argued that vertical integration provides it with greater control, potentially helping the company to avoid issues.

Joby’s initial timeline assumed FAA certification flight testing in 2022, demonstration services and mass production in 2023 and the launch of commercial services in 2024. The company now appears to be something like 2-3 years behind on this timeline though. Joby is making progress, having completed the first three stages of certification and was the first UAM company to do so. Joby is now proceeding to submitting test plans and conducting for-credit tests in stage four. Testing will progress from components to systems and finally aircraft, with Joby recently starting to submit its first system-level test plans. While the certification process will hopefully proceed smoothly and be completed in a timely manner, there is really no way of knowing if issues will come up that end up causing significant delays.

Joby recently began testing with a pilot on board and has now completed over 100 inhabited flights. 10 pilots have also flown Joby aircraft through transition. The company believes that early testing has demonstrated that its aircraft have the same infrastructure requirements as similarly sized aircraft, allowing it to leverage existing infrastructure. Joby also recently completed its first eVTOL flight in New York, demonstrating the maturity of its aircraft program. Joby’s pre-production prototype aircraft logged more than 1,500 flights and 33,000 miles.

Manufacturing

Joby has partnered with Toyota to support manufacturing at scale. This reduces both capital requirements and the risk involved with setting up complex manufacturing operations. In preparation for scaled manufacturing a site has been acquired in Ohio and in-house tooling developed. In the meantime, Joby has a facility in California which is supporting production for testing and certification. Joby is doubling the footprint of this facility and expects to be able to produce up to 25 aircraft per year at this location while its Ohio facility is setup. The company is targeting a production run rate of 1 aircraft per month by the end of this year. Two production prototype aircraft have already been completed and a third is expected by the time of the second quarter call.

UAM Service

While commercialization is still some way off, Joby expects to be first to market. This is a positive, if for no other reason than it minimizes cash burn, but I don’t believe it will provide a meaningful advantage. Joby expects to start with a limited rollout, creating scale in a small number of locations before adding new cities. Likely early operating areas in the US include:

- Los Angeles

- The Bay Area

- Miami

- The Tri-State Area

Joby is working with Delta on opportunities related to Delta’s hubs at JFK, LaGuardia and LAX. This is in addition to Joby’s partnership with Clay Lacy to support the development of its LA Network. The company also recently announced partnerships in the New York City region to support the installation of charging infrastructure and Nomura is supporting the development of a Tokyo Network.

Joby also plans on launching air taxi services in the UAE by early 2026. The company has signed an agreement with Dubai’s Road and Transport Authority that provides an exclusive right to operate air taxis in Dubai for six years. Joby has also signed an agreement with Skyports, who will initially develop and operate 4 vertiport sites across Dubai. The agreement grants Joby exclusive rights to operate air taxis in the Emirate for six years and includes financial support for initial operations.

Joby acquired Uber Elevate in January 2021, which appears to have been an attempt to reduce go-to-market risk. The company expects to partner with Uber to generate demand in the US, with Joby appearing in the Uber app on a non-exclusive basis.

OEM Sales

On the OEM front, Joby has already delivered eVTOL aircraft to the US Air Force. Joby will commit at least two more aircraft to the Department of Defense as part of its existing contract. Joby has in excess of $40 million of contracts secured with an estimated $120+ million in progress.

Financial Analysis

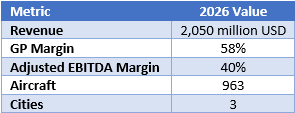

At the time of its SPAC, Joby was guiding to roughly $2 billion revenue in 2026. Even though commercialization has pushed out, revenue is still expected to rapidly ramp over the next few years. Analysts currently have Joby pegged for around $120 million revenue in 2026 and expect the company to reach $2.5 billion revenue in 2029.

Joby’s $2 billion revenue estimate assumed close to 1,000 aircraft operating for 12 hours per day, performing around 12.4 million total flights per year with an average trip length of 24 miles, a load factor of 2.3 passengers per trip and generating $3 revenue per seat mile.

Table 1: Joby Financial Target from SPAC Presentation (source: Created by author using data from Joby)

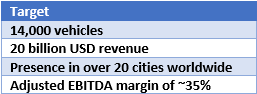

Longer term, the company expects to have approximately 14,000 vehicles operating in over 20 cities globally. This would presumably mean in excess of 10 million flights annually in busier cities.

Table 2: Joby 10 Year Targets (source: Created by author using data from Joby)

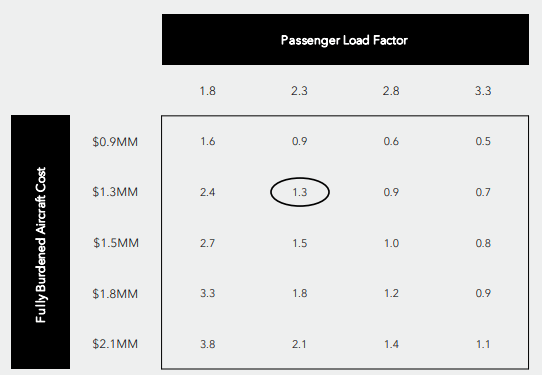

Utilization is an improvement driver of UAM economics, along with aircraft production cost. Joby has designed its aircraft to carry four passengers to optimize unit economics. The company is assuming a fully loaded manufacturing cost of $1.3 million per aircraft with an average useful life of 50,000 flight hours.

Joby’s numbers suggest a gross profit margin approaching 60% and an EBIT margin in the low 20% range. Margins will also be heavily dependent on market structure though, and in general passenger transportation is not a high-margin business. Unless competition is minimal, I would expect Joby’s margins to be in the low teens or even single digit percent range.

Figure 3: Impact of Load Factor and Aircraft Cost on Payback Period (source: Joby)

Cash burn and the path to commercialization are critical at this point, as existing investors risk being significantly diluted, even if Joby ends up being a success. Joby currently has a little over $900 million of cash and cash equivalents on its balance sheet, providing it with a sizeable runway. The company expects to burn approximately $440-470 million cash in 2024. Despite this, there is a high probability that the company will need to raise capital before it reaches breakeven, particularly if commercialization continues to be pushed back.

Conclusion

The lower noise levels generated by eVTOL aircraft should support growth of the UAM market in coming years. While lower prices could also stimulate demand, the impact of this may be less than is widely expected. UAM is likely to be a sizeable market but there is still a large amount of uncertainty at the moment regarding factors like aircraft performance, costs, safety, supply scalability and demand. Even if the UAM market does end up generating hundreds of billions of dollars revenue, like is widely anticipated, competition may limit the value that is captured by companies like Joby.

While there are questions about the company’s long-term value, I expect Joby’s near-term share price movements to be dictated by its need to access additional capital and its progress towards certification. Sufficiently rapid progress could see Joby’s valuation rise and allow the company to raise capital on favorable terms. Conversely, significant delays could pressure Joby’s share price and make it hard for the company to continue financing operations.

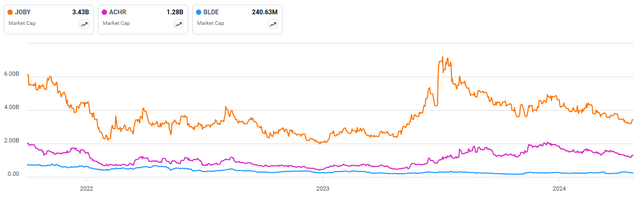

I can see a successful company in this market eventually being worth something like $10-20 billion, which given the risk and the long timeline involved, makes Joby fairly fully valued already. As a reality check on the market, it is worthwhile considering Blade’s valuation. Blade’s enterprise value is only a little over $100 million, despite the company having exposure to the commercialization of eVTOL aircraft through its UAM service. This could make Blade the best way to gain exposure to UAM unless a dominate player in manufacturing begins to emerge.

Figure 4: Joby Market Capitalization (source: Seeking Alpha)

from Finance – My Blog https://ift.tt/KaAph6O

via IFTTT

0 Comments